注意事項

前往結尾以下載完整範例程式碼。 或透過 JupyterLite 或 Binder 在您的瀏覽器中執行此範例

非負最小平方#

在此範例中,我們將線性模型擬合到迴歸係數上具有正約束的條件,並將估計的係數與經典線性迴歸進行比較。

# Authors: The scikit-learn developers

# SPDX-License-Identifier: BSD-3-Clause

import matplotlib.pyplot as plt

import numpy as np

from sklearn.metrics import r2_score

產生一些隨機資料

np.random.seed(42)

n_samples, n_features = 200, 50

X = np.random.randn(n_samples, n_features)

true_coef = 3 * np.random.randn(n_features)

# Threshold coefficients to render them non-negative

true_coef[true_coef < 0] = 0

y = np.dot(X, true_coef)

# Add some noise

y += 5 * np.random.normal(size=(n_samples,))

將資料分割為訓練集和測試集

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.5)

擬合非負最小平方。

from sklearn.linear_model import LinearRegression

reg_nnls = LinearRegression(positive=True)

y_pred_nnls = reg_nnls.fit(X_train, y_train).predict(X_test)

r2_score_nnls = r2_score(y_test, y_pred_nnls)

print("NNLS R2 score", r2_score_nnls)

NNLS R2 score 0.8225220806196525

擬合 OLS。

reg_ols = LinearRegression()

y_pred_ols = reg_ols.fit(X_train, y_train).predict(X_test)

r2_score_ols = r2_score(y_test, y_pred_ols)

print("OLS R2 score", r2_score_ols)

OLS R2 score 0.7436926291700353

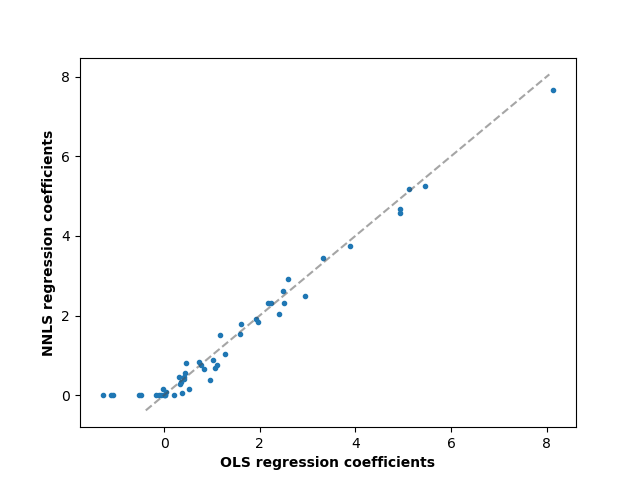

比較 OLS 和 NNLS 之間的迴歸係數,我們可以觀察到它們高度相關 (虛線是恆等關係),但非負約束會將某些係數縮小為 0。非負最小平方本質上會產生稀疏結果。

fig, ax = plt.subplots()

ax.plot(reg_ols.coef_, reg_nnls.coef_, linewidth=0, marker=".")

low_x, high_x = ax.get_xlim()

low_y, high_y = ax.get_ylim()

low = max(low_x, low_y)

high = min(high_x, high_y)

ax.plot([low, high], [low, high], ls="--", c=".3", alpha=0.5)

ax.set_xlabel("OLS regression coefficients", fontweight="bold")

ax.set_ylabel("NNLS regression coefficients", fontweight="bold")

Text(55.847222222222214, 0.5, 'NNLS regression coefficients')

腳本的總執行時間: (0 分鐘 0.068 秒)

相關範例